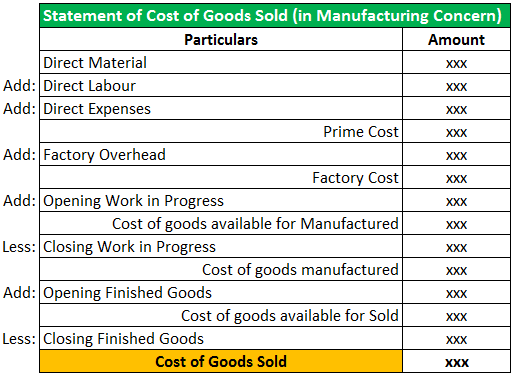

We had a beginning inventory of $50,000 which was shown on last year’s balance sheet. And during the year, we have made a total of $200,000 in purchases. Likewise, we can calculate the cost of goods sold with the formula of the beginning inventory plus purchases minus the ending inventory.

Cash Flow vs Revenue: Which Metric Matters More for Your Ecommerce Business?

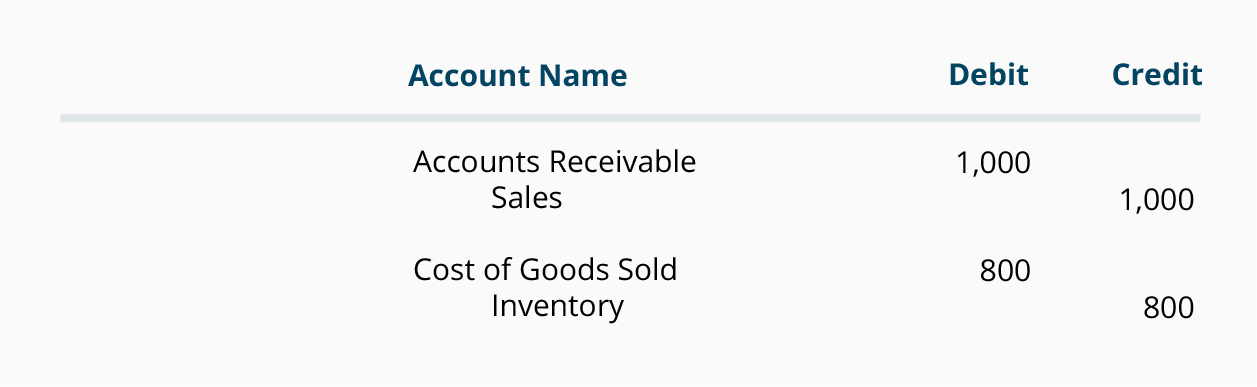

It will consist of debits made to your COGS expense account and credits made to both your purchases account and inventory account. Perpetual inventory system is a technique of maintaining inventory records that provides a running balance of cost of goods available for sale and cost of goods sold for a period. Under this system, no purchases account is maintained because inventory account is directly debited with each purchase of merchandise. Under perpetual inventory system, the expenses that are incurred to obtain merchandise inventory are added to the cost of merchandise available for sale.

Method Two

Yes, your cost of goods sold should be included on your income statement for the reporting period. When listed in the revenue section, it allows you to calculate gross margin before diving into expenses. If the firm is a manufacturer, it must maintain some inventory of raw materials and work-in-process in order to keep the factory running.

- By determining a reorder point, the business avoids running out of inventory and can continue to fill customer orders.

- When listed in the revenue section, it allows you to calculate gross margin before diving into expenses.

- LIFO (Last-In, First-Out), on the other hand, results in higher COGS and lower net income.

- When prices are going up, FIFO (First-In, First-Out) results in lower COGS and higher net income.

- For other business structures, the deduction still applies but might be reported in different forms corresponding to their tax filing requirements.

- An item damaged before it’s sold means a debit to an account specific to Loss from Damaged Inventory.

Cost of goods sold under perpetual inventory system

We use the perpetual inventory system in our company to manage the merchandise goods. If you use accounting software, look for features that automate inventory transactions. If you are dealing with a unique situation, consider consulting with an accountant or professional bookkeeper. If you make any inventory adjustments like write-offs or shrinkage, you create another journal entry to reflect each of these changes.

High COGS can squeeze margins, leaving less net income, while effectively managing COGS can boost profit by keeping these costs in line with revenue. When you purchase materials, credit your Purchases account to record the amount spent, debit your COGS Expense account to show an increase, and credit your Inventory account to increase it. As a brief refresher, your COGS is how much it costs to produce your goods or services.

COGS journal entry examples

By determining a reorder point, the business avoids running out of inventory and can continue to fill customer orders. If the company runs out of inventory, there is a shortage cost, which is the revenue lost because the company has insufficient inventory to fill an order. An inventory how to record cost of goods sold journal entry shortage may also mean the company loses the customer or the client will order less in the future. The goal of the EOQ formula is to identify the optimal number of product units to order. If achieved, a company can minimize its costs for buying, delivery, and storing units.

For the entry, you’ll need the number of items sold and how much each one costs to produce or purchase. This expense is part of inventory costs and directly affects the value of goods sold. These ledger reflections serve as a financial narrative, detailing how production elements translate into accounting stories on paper.

That may include the cost of raw materials, cost of time and labor, and the cost of running equipment. Selling the item creates a profit, but a portion of that profit was lost, due to the cost of making the item. In this journal entry, the credit of $10,000 in the inventory account comes from the balance of the beginning inventory ($50,000) minus the balance of the ending inventory ($40,000). And the purchases account of $200,000 will be cleared to zero when we close the company’s accounts at the end of the accounting period.

If inventory increases, it suggests fewer sales, leading to a lower COGS. When inventory decreases, this indicates more sales have occurred, resulting in a higher COGS. It’s the movement of inventory, driven by sales, that shapes the COGS value. Mastering COGS recording is not merely about getting the books right; it’s a strategic skill that propels informed decision-making and financial robustness.

COGS is your beginning inventory plus purchases during the period, minus your ending inventory. When prices are going up, FIFO (First-In, First-Out) results in lower COGS and higher net income. LIFO (Last-In, First-Out), on the other hand, results in higher COGS and lower net income.